Greece’s Domestic and International Issues

By Amber Abdul

Monetary twin to the American Experiment, the Euro Experiment was launched by the European Economic and Monetary Union (EMU) on January 1, 1999, to facilitate economic stability, growth, and integration amongst members of the European Union (EU). With 19 countries now a part of the EMU, debt incurred by member nations is managed by an extensive system: the Economic and Financial Affairs Council (ECOFIN), the European Council (EC) and the European Central Bank (ECB) among others (Ardagna & Caselli 291). Greece, an EMU member since 2002, has undergone a series of debt problems from 2009 to 2011 and raised serious concerns within ECOFIN, EC, and ECB. This paper thus explores to what extent Greece’s response to its debt crises were marred by the passiveness of EMU institutions and of the Greek government.

Inklings of the weakness of the Greek government could be seen in the conversion process to the euro. On January 1, 2002, Greece converted from the drachma to the euro, with 340.75 drachmas equating 1 euro (Malaby 43). Greece had converted to the euro in hopes of eliminating exchange rate uncertainty, lowering transaction costs, and reducing ambiguity when trading with other European nations (Galanos et al Expected Collapse 263). This conversion was accompanied by a mass information campaign. Conversion calculators became a popular commodity, allowing the Greek populace to constantly rethink their currency in terms of euros (Malaby 43). However, the solution of the conversion calculator became the creator of new problems, as it did not round the drachma. The government had set strict rounding guidelines for the drachma to euro conversion, yet only imposed such restrictions on public institutions (Malaby 49). This left a regulatory vacuum in the private sector, allowing businesses to decide for themselves who (buyer or seller) bore the burden of rounding. There were thus asymmetries concerning the interpretation of the drachma across businesses, pointing to the passivity of the Greek government. The conversion process ended on February 28, 2002, despite continuing asymmetries and lack of regulatory power. The process occurred in less than a month, showing a rushed joining of the EMU. Thus, the path of adopting the euro was characterized by hastiness and passiveness of the Greek government.

Greece’s entry into the EU was envisioned to give it economic benefits through the reduction of transaction costs, elimination of exchange rate uncertainty, a boost in trade, monetary stability and greater external liquidity. However, weaknesses in the Greek economy and the government’s lack of fiscal discipline, even within the constructs of the tighter controls required for EMU membership, contributed to the debt crises experienced between the years of 2009 and 2011. For example, inflation had consistently been around 50% higher than the Eurozone average, generating an increase in Greek prices by 32.8% (Galanos et al Expected Collapse 264). This created large discrepancies in pricing across eurozone countries, despite the usage of similar currencies. Joining the EMU allowed for the liberalization of Greece’s capital and provided an unimpeded flow of capital and a reduction in borrowing rates (Galanos et al Expected Collapse 264). It should thus come as no surprise that easy access to funds, coupled with the lack of effective oversight and lack of fiscal discipline would eventually lead to problems.

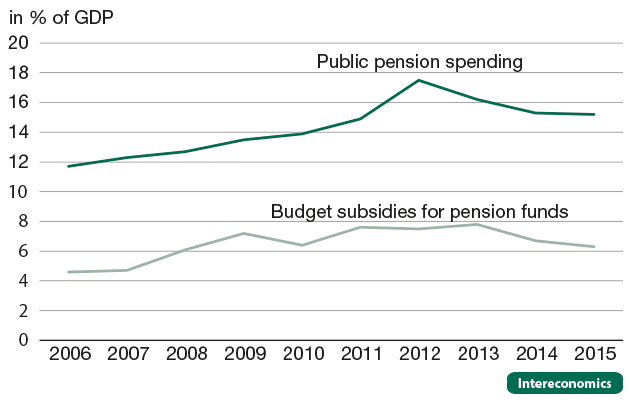

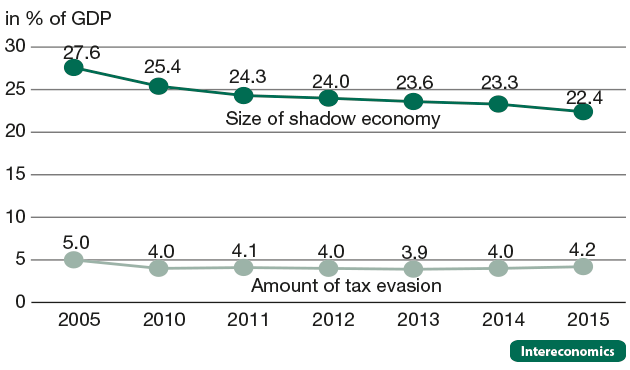

The political structure of Greece is fertile ground for debt creation and mismanagement. Greece follows a “majoritarian” structure in its electoral politics. In order to form a majority, parties must rely on forming coalitions on multiple issues that may not contribute to a stable economy. Such coalition-forming fosters the creation of clientelist networks that would attract new votes while securing the loyalty of partisan voters (Kovras & Loizides 5). Clientelist practices of the political parties also bled into the broader area of government. Supporters of government officials would be rewarded with public jobs, with 12.8% (about 692,000 people) of its working population being employed by the government (Kovras & Loizides 5). These workers are entitled to large pension funds, which the government did not have the budget to pay yet continued to spend (see Figure 7). In addition, regions considered electorally critical were given informal “tax breaks”, in which government officials relaxed tax audits which contributed to tax evasion (Kovras & Loizides 7). Tax evasion was thus implicitly legal, and such lack of tax collection and oversight generated a relatively large shadow economy that undermined GDP growth (see Figure 8). With government revenue deliberately undermined for political gain, the Greek government’s misplaced priorities contributed to the looming debt crisis.

It is important to note that the inefficiencies that arose during and after the conversion to the euro happened under the watchful eye of the EMU and its supporting institutions. Under the EMU’s Stability Pact of maintaining a budget deficit under 3% of GDP, Greek fiscal deficits remained wholly above the threshold, generating ever-increasing public debt (Galanos et al Expected Collapse 266). Although Greece was placed under EU surveillance in 2006-2007 due to its divergence from accepted economic practices and its debt, the nation continued to waste resources in following years (Galanos et al Expected Collapse 264). Greece, it appeared, had downplayed or miscalculated its GDP growth and other economic measures, without the overall EMU being aware. In 2009, the newly elected government had reported that the overall budget deficit was 12-13%, nearly double what had been reported by the previous government (Ardagna & Caselli 293). This points to a lack of oversight by the EMU and its supporting institutions for their member states. Such lack of discipline was especially exacerbated under the bailout plants of May 2010 and July 2011, in which Germany and the ECB were at odds on whether the public or private sector of other EMU states would bear the burden of bailing Greece out (Ardagna & Caselli 311). Internal disagreements due to different political and economic gains thus slowed the process by which Greece could receive aid.

As Greece shares a currency with 18 other countries, the response to its debt can partly be measured by the intentions of the institutions which support it. ECOFIN is composed of 27 financial ministers who hail from each member state of the EU. Their purpose is to coordinate and evaluate the economic and financial policy of its member states. It is thus made up of politicians whose decisions may be influenced by their own government and/or electorate (Ardagna & Caselli 291). EC, like ECOFIN, is headed by 27 government officials. These officials gather to set the political priorities of the overall EU, creating an added possibility that they are animated by the electoral incentives of their respective countries. ECB, the central bank of the Eurozone, is owned by each central bank of the 27 member states of the EU. Its task largely centers on price stability and stabilizing the monetary policy of member nations. Because ECB is owned by each central bank, it is more easily removed from political incentives. Taken together, however, it is clear that Greece exists within a political union as much as an economic union. Greece’s journey to debt alleviation is thus aided by organizations whose political incentives may hinder their ability to provide aid.

Greece thus exists within an international web that is fraught with competing political interests. Domestically, Greece faces a weak government dominated by vested interests coupled with a lack of policy prioritization for its debt burden. The beleaguered country faces a long road ahead that will involve harsh austerity measures and significant hardship. However, it is in a better position to do so as part of the EMU rather than if it was alone. There must be improvement within the political sphere of both the EMU and Greece itself for the country to progress. The Greek populace must hold its government accountable for its shortcomings, even if it means forgoing short-term “benefits” (such as tax breaks) for long term progress (debt alleviation). The EMU must closely monitor its member nations from the moment they become an EMU member, keeping track of budgets, debt, and must create comprehensive debt relief plans that are as apolitical as possible. Such demands will be hard to satisfy, but if both the EMU and Greece collaborate in their reforms significant improvements can be made.

Fig 7: Galanos et al Greece’s Systemic Weaknesses 299

Fig 8: Galanos et al Greece’s Systemic Weaknesses 300

Amber Abdul is a First-Year at Tufts University

Image Courtesy Pixabay at Pexel.

Works Cited

Ardagna, Silvia, and Francesco Caselli. “The Political Economy of the Greek Debt Crisis: A Tale of Two Bailouts.” American Economic Journal: Macroeconomics, vol. 6, no. 4, 2014, pp. 291–323. JSTOR, www.jstor.org/stable/43189946. Accessed 10 May 2021.

“Economic and Financial Affairs Council Configuration (Ecofin).” Consilium, Council of the EU, 19 Jan. 2021, www.consilium.europa.eu/en/council-eu/configurations/ecofin/.

European Central Bank. “About.” European Central Bank, 22 Jan. 2021, www.ecb.europa.eu/ecb/html/index.en.html.

“The European Council.” Consilium, European Council, 20 Apr. 2021, www.consilium.europa.eu/en/european-council/.

Galanos, George, et al. “Greece and the Euro: The Chronicle of an Expected Collapse.” Intereconomics, 1 Jan. 1970, www.intereconomics.eu/contents/year/2011/number/5/article/greece-and-the-euro-the-chronicle-of-an-expected-collapse.html.

Galanos, George, et al. “How Greece’s Systemic Weaknesses Limited the Effectiveness of the Adjustment Programmes.” Intereconomics, 1 Jan. 1970, www.intereconomics.eu/contents/year/2017/number/5/article/how-greeces-systemic-weaknesses-limited-the-effectiveness-of-the-adjustment-programmes.html.

Kovras, Iosif, and Neophytos Loizides. “The Greek Debt Crisis and Southern Europe: Majoritarian Pitfalls?” Comparative Politics, vol. 47, no. 1, 2014, pp. 1–20. JSTOR, www.jstor.org/stable/43664340. Accessed 10 May 2021.

Malaby, Thomas M. “The Currency of Proof: Euro Competence and the Refiguring of Value in Greece.” Social Analysis: The International Journal of Social and Cultural Practice, vol. 47, no. 1, 2003, pp. 42–52. JSTOR, www.jstor.org/stable/23170067. Accessed 10 May 2021.